THE HOUSING MARKET IN LATE 2024: INSIGHTS FOR HOMEBUILDERS

November 8, 2024

The housing market remains complex, with notable dynamics affecting both supply and demand. As of late 2024, there are key trends in employment, inflation, interest rates and inventory that homebuilders must navigate to stay competitive. Here’s a look at the state of the single-family housing market, based on recent insights from Ali Wolf, Chief Economist at Zonda.

ECONOMIC OVERVIEW

EMPLOYMENT AND INFLATION

Despite the unemployment rate recently rising to 4.1%, the job market remains relatively strong, averaging 200,000 new jobs per month. This employment stability has influenced the Federal Reserve’s cautious approach toward interest rate adjustments, given that high employment traditionally supports consumer spending and housing demand.

On the inflation front, while economists celebrate the deceleration of inflation toward the Fed’s 2% target, high prices persist across many sectors, leaving consumers focused on immediate costs rather than on inflation’s deceleration. As a result, consumers are becoming more selective with spending—prioritizing essentials, shopping for deals or delaying non-essential purchases. This pullback affects housing as buyers delay big-ticket purchases as they hope for lower prices or rates in the future.

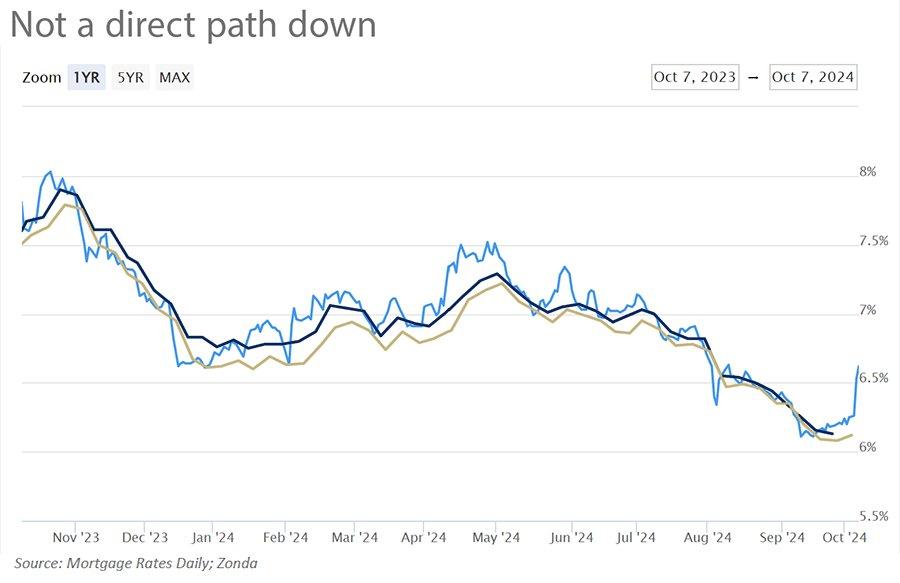

INTEREST RATES

The Federal Reserve aims to gradually reduce the federal funds rate, aiming to eventually reach a “neutral” rate (believed to be between 2.5% and 3.5%), which is critical to stabilizing the market. The Fed’s projections suggest that the federal funds rate will continue to decrease slowly, but another rate cut could happen by the end of the year, and mortgage rates are forecasted to average in the high 5% range by 2025.

However, mortgage rates have shown notable volatility, with recent fluctuations tied to investor sentiment, economic strength and federal policy outlooks. It can be tricky to forecast because, for example, since the Federal Reserve cut rates in September, interest rates have gone up, which seems confusing to many people. Remember that investors are the ultimate driver of interest rates, and since the economy is stronger than initially expected, that put some upward pressure on rates.

MARKET DYNAMICS IN HOUSING

INVENTORY AND SALES TRENDS

Across the housing landscape, existing home sales in 2024 are poised to be the lowest transaction levels since 1995, a trend driven by high prices and elevated mortgage interest rates. However, inventory has grown, with active listings up about 35% year-over-year, marking a high since the pandemic. Levels are still down compared to pre-pandemic (approximately 25% compared to 2019), though this varies significantly by region. Areas in the Northeast, California and Midwest still have tight inventory–down 20, 40, or 60% compared to pre-pandemic, while regions like Texas, Florida, Arizona and Colorado have seen inventory levels rise.

Homebuilders have continued to benefit from limited competition with resale homes, thanks in part to the “lock-in effect,” where homeowners are reluctant to sell and reset to a higher mortgage rate. While early in the year, 80% of builders reported minimal resale competition, this has declined to around 50% as inventory gradually increased in some regions. Builders are utilizing incentives, like mortgage rate buydowns and closing cost assistance, to draw in buyers—a strategy expected to remain key given the affordability challenges in today’s market.

Housing sales are following the normal seasonal trends. September sales came in lower than what they were in February, March and April, but that is expected because the spring selling season typically does see higher sales volume. Nationally, Zonda found that the new home market in September overperformed for the ninth consecutive month. In 66% of the nation’s top markets, the markets overperformed in September compared to only 14% that were underperforming.

Importantly, the data doesn’t always match the sentiment on the ground. The sales numbers don’t take into consideration how difficult it can be to sell a home or whether price cuts or other incentives were included. We know incentives are still an active aspect of the housing market with builders often offering mortgage rate buydowns, funds toward closing costs and flex dollars to help make their sales.

HOUSING STARTS

Housing starts, driven in part by builder confidence in specific regions, have increased year-over-year, with Texas and Florida leading in new construction activity. Dallas, Houston, San Antonio, Austin, Orlando and Tampa are among the top 8 markets nationally for housing starts, illustrating a strong demand for new housing in Texas and Florida. Texas and Florida represent 40% of the top production markets in the country. However, some regions like Denver and Seattle, while experiencing demand, face constraints such as high costs and limited developable land, slowing start growth.

Nationally, builders are increasingly focusing on “spec” homes (homes built without specific buyers) to respond to expected demand shifts. As of the second quarter, housing starts were up year-over-year in all top 25 markets, with 20 of these markets also exceeding pre-pandemic 2019 levels.

Builders report plans to increase single-family housing starts in 2025, with a forecasted growth range of 1-3%. This optimism reflects expectations for easing interest rates and pent-up buyer demand. Land and lot supply is gradually improving, especially in regions that saw supply tighten in the last few years.

REMODELING TRENDS

The remodeling sector, while facing headwinds from lower mobility and depleted savings, is expected to rebound. Many homeowners are increasingly dissatisfied with their current homes and are considering remodeling as a means to improve their living space.

Additionally, accumulated home equity (estimated to be worth approximately $12 trillion) since 2020 and a high volume of untapped HELOCs provide a significant resource for future remodeling spending. Zonda’s forecast indicates a potential V-shaped recovery in remodeling as homeowners tap into this equity over the next year.

KEY TAKEAWAYS FOR HOMEBUILDERS

For homebuilders looking to finish 2024 strong and aiming for 2025, both challenges and opportunities are abundant. With a cautious Federal Reserve policy, interest rates may stabilize and possibly decline, potentially easing some of the affordability concerns that keep buyers on the sidelines. Additionally, the anticipated uptick in remodeling activity could present growth avenues for builders who provide renovation services. However, high competition, especially in regions with abundant new listings, underscores the importance of strategic pricing, effective incentives and a deep understanding of local market trends.

As the economy and housing market continue to evolve, homebuilders should remain adaptable, balancing short-term conditions with long-term demand fundamentals to position themselves for success in a dynamic environment.